Employer-sponsored health insurance represents a substantial component of total compensation paid by firms to many workers in the United States. Such costs have climbed by close to 20 percent over the past five years. Indeed, the average annual premium for employer-sponsored family health insurance coverage was about $27,000 in 2025—roughly equivalent to the wage of a full-time worker paid $15 per hour. Our February regional business surveys asked firms whether their wage setting decisions were influenced by the rising cost of employee health insurance. As we showed in our companion post, respondents reported an average increase in such costs of more than 13 percent this year. Businesses providing insurance to their workers indicated that absent these cost increases, they would have raised wages by roughly an additional percentage point, on average, suggesting that rising health insurance costs resulted in a drag on wage growth for workers at these firms.

Wage Growth Continues to Slow

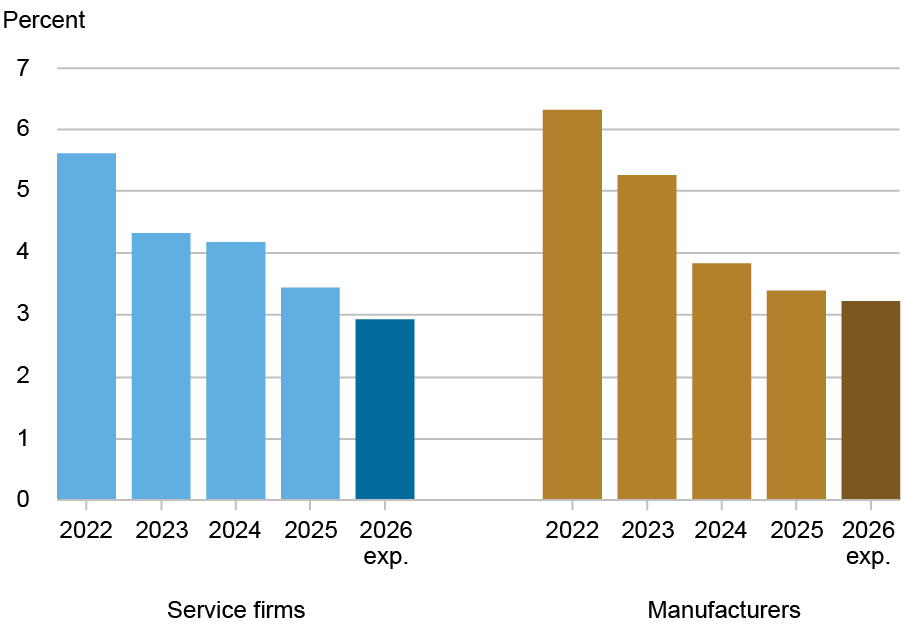

Our February regional business surveys asked firms in the New York-Northern New Jersey region about past and expected changes in their wages, questions which we asked in prior years. As shown in the chart below, wage growth has slowed every year since 2022, likely reflecting the effects from lower inflation pressures and a cooling of the labor market over the last few years. Among service firms, the average wage increase slowed from 5.6 percent in 2022 to 3.4 percent in 2025, and among manufacturers, from 6.3 percent in 2022 to 3.4 percent in 2025. Wage growth is expected to slow further to 2.9 percent among service firms and to 3.2 percent among manufacturers in the year ahead.

Wage Growth Has Slowed, And Is Expected to Slow Further

Note: These averages represent a trimmed mean; the highest 5 percent and the lowest 5 percent of responses are excluded.

Rising Employee Health Insurance Costs Dampening Wage Growth

Though wage growth has slowed in recent years, wages are only one part of total labor costs. About three-quarters of service firms in our surveys and 90 percent of manufacturers provide health insurance to their workers. And while wage growth has been slowing since 2022, health insurance costs have been rising sharply. According to the Kaiser Family Foundation, health insurance costs increased by about 6 percent in 2025, and were projected to rise by 11 percent in 2026, similar to the more than 13 percent increase businesses in our surveys reported as their policies renewed. Based on information provided by insurers, these higher insurance costs have been driven in large part by the increased cost of hospitalization and physician care, as well as the high cost of providing GLP-1 and other prescription drugs.

How have firms managed these substantial cost increases? Some firms reported that they passed a portion of the cost increases on to their customers by raising prices, while others absorbed them through reduced profit margins. A number of firms reported that they had offset at least some of the increased costs by reducing health insurance coverage to workers or by increasing employee contributions. However, many firms responded to these higher costs by reducing the wage increases they gave to their workers.

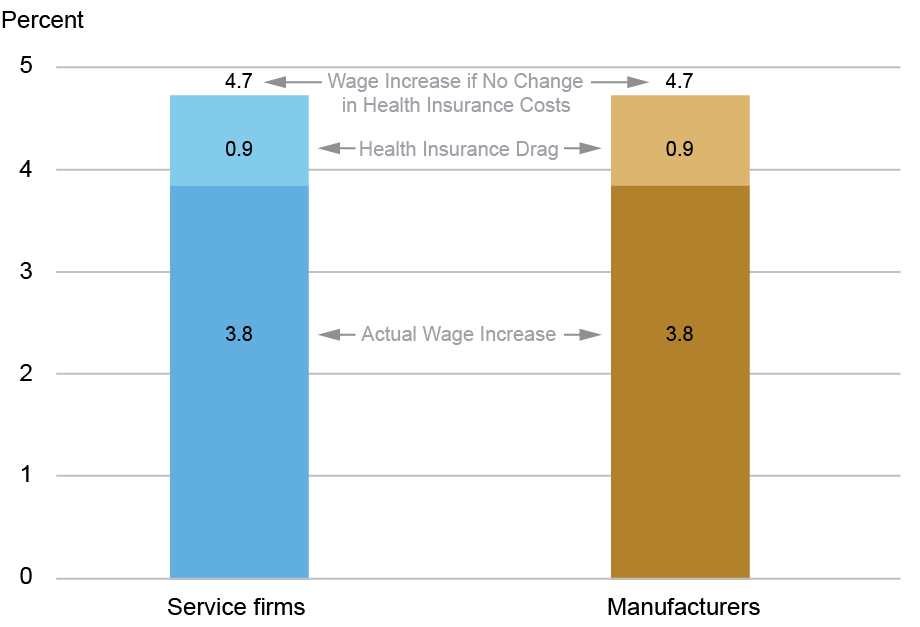

In order to better understand the relationship between rising health insurance costs and wages, we asked businesses who saw health insurance cost increases what wage growth would have been in a world where, hypothetically, such costs hadn’t gone up. Though this hypothetical likely does not represent a realistic counterfactual given existing healthcare cost trends, it helps illuminate the extent to which some firms are managing cost pressures by modifying wages in response to higher health insurance costs. Results of this counterfactual are shown in the chart below.

Wage Increases Would Be Higher Absent Rising Employee Health Insurance Costs

Notes: These averages represent a trimmed mean; the highest 5 percent and the lowest 5 percent of responses are excluded. Figures are based on firms reporting an increase in employee health insurance costs over the past year.

Among those businesses experiencing an increase in employee health insurance costs, the average wage increase over the past year was 3.8 percent for both service firms and manufacturers, slightly higher than the 3.4 percent reported among all firms in the surveys. However, these firms reported that the average wage increase they would have given to their workers if health insurance costs had not gone up was about 4.7 percent. Thus, wage growth for workers at these service and manufacturing firms would have been about one percentage point higher, on average, if health insurance costs had held steady—the equivalent of a 20 percent drag on wage growth. As such, there does appear to be a connection between rising health insurance costs and wage growth among many firms.

Labor Costs Are Rising Faster Than Wage Increases Suggest

Since health insurance expenditures represent a significant portion of total labor compensation for many firms, the true cost of employing workers at these firms has been climbing faster than wage increases alone suggest, potentially squeezing profit margins and making labor more expensive than it appears from the wage bill alone. While not every firm provides health insurance to its workers, it appears that rising employee health insurance costs are increasing cost pressures for some businesses, limiting wage growth for many workers.

Jaison R. Abel is head of Microeconomics in the Federal Reserve Bank of New York’s Research and Statistics Group.

Richard Deitz is an economic policy advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Nick Montalbano is a data analytics specialist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Jaison R. Abel, Richard Deitz, and Nick Montalbano, “Are Rising Employee Health Insurance Costs Dampening Wage Growth?,” Federal Reserve Bank of New York Liberty Street Economics, March 4, 2026, https://doi.org/10.59576/lse.20260304b

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).